CFO GROUP INTEGRATED SERVICES

Singapore Corporate Tax Guide

CMO Media Lab Pte Ltd • January 10, 2022

Every corporate company director in Singapore needs to understand the personal income tax requirements for their specific situation. This article will help guide you through what is considered personal income tax and how to pay it as a corporate company director.

- What Is Considered Personal Income Tax for Company Owners?

- Who is required to pay corporate taxes in Singapore?

- What are the advantages of being a tax-resident company in Singapore?

- When Should I File My Corporate Tax?

- Tax Penalties for Incorrect Tax Returns

- Income tax filing due date

- Income tax basis period

- Withholding tax

- Singapore tax treaties

Source from: https://osome.com/sg/blog/a-guide-to-income-tax-for-foreign-company-owners-and-directors-in-singapore/

What Is Considered Personal Income Tax for Company Owners?

Company Founders or Business Owners

Whether foreign or local, resident or non-resident, entrepreneurs are regarded as self-employed in Singapore and are the sole proprietors of their commercial enterprises. If you're self-employed, you must include your company revenue when figuring up your taxes. Paying company taxes is treated the same as paying personal income taxes for this rule. Self-employed people can benefit from the Pre-filling of Self-Employed Income, which sends information about your earnings to the tax system on your behalf automatically.

Directors of businesses

Directors of a private limited business paid monthly are treated as employees for tax purposes. They must pay income tax on their gross compensation on a calendar year-to-year basis. Form IR8A issued by IRAS must be completed.

Apart from their pay, company directors frequently receive perks such as automobile allowances, housing expenditures, and company-provided housing. Therefore, appendix 8A must be filed together with Form IR8A if you or any of your company's employees receive benefits.

Only the Income You Earned in Singapore is Taxable

Income tax applies to any money earned in Singapore.

If you earn income from outside of Singapore, your income is taxable only if:

- You receive it through partnerships in Singapore, OR

- Traveling outside of Singapore is required of you as a part of your employment responsibilities in Singapore.

Do I have to pay any personal income tax if I'm a company director?

The income tax you pay depends on:

- Your tax resident

- The total amount of chargeable income that you earn

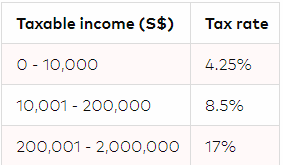

A Singaporean corporation can expect to pay 17% tax on its chargeable income.

Who is required to pay corporate taxes in Singapore?

The Revenue Tax Act requires all corporations to participate, regardless of tax residence status, to pay a chargeable amount of corporate taxes on any income obtained from Singapore or foreign income transferred to Singapore.

On the other hand, companies based in Singapore benefit from a number of advantages over those based elsewhere.

Source from : https://singaporelegaladvice.com/law-articles/singapore-corporate-tax-guide-tax-rate-filing-procedure/

What are the advantages of being a tax-resident company in Singapore?

The benefits enjoyed by tax-resident companies include:

- A Singapore tax-resident company may benefit from the Avoid Double Taxation Agreements (DTAs) with other nations, which means it is not subject to double taxation on certain earnings. This implies that the firm can claim tax exemption or reduction in any income that has already been taxed in a foreign country. The company may also claim tax exemptions or deduct tax set-offs in the foreign country.

- A Singapore tax resident company might be eligible for tax-exemptions on foreign dividends, foreign branch profits, and service revenues from other nations if such income was previously subject to corporate taxation in the foreign countries. To qualify for such exemptions, the foreign country in question must have a corporate tax of at least 15%, and the Inland Revenue Authority of Singapore (IRAS) considers the exemption to be beneficial to the company.

- A Singapore-based firm can benefit from the Start-Up Tax Exemption Scheme for the first three years without paying any taxes. Newly formed firms are eligible for a tax exemption of 100% on their first S$100,000 chargeable income and a further 50% tax exemption on their subsequent S$200,000 chargeable revenue under this programme. (From YA 2020, the tax exemption will be decreased to 75% on the first S$100,000 of chargeable income and 50% on the next S$100,000 of chargeable income.)

In addition to the corporate tax rate, all Singapore companies are also required to pay withholding tax (tax which must be paid on payments to foreign companies) when they make payments regarding certain categories of services to non-resident companies.

When Should I File My Corporate Tax?

From YA 2020, all Singapore resident companies are required to e-File their corporate tax documents by 30 November. Physical filing is not accepted.

Late filing of corporate tax is an offence. The company’s officers (e.g. their directors) may be prosecuted in court.

In court, the company’s officers and the company may be fined up to $10,000 and $1,000, respectively. However, the company may be allowed to settle its fine through paying a composition amount of between $200 and $1,000.

In any case, the company will still have to file its outstanding corporate taxes documents.

Tax Penalties for Incorrect Tax Returns

There is a possibility that IRAS might apply the following sanctions if the Income Tax Returns have been filed incorrectly without any purpose to avoid paying taxes:

Financial penalties of up to 200% of the tax undercharged;

- Fines of up to S$5,000; and/or

- Imprisonment of up to 3 years.

Corporate Tax Penalties for Late or Non-Payment

Failure to pay assessed corporate tax on time may result in a 5% penalty, followed by a 1% penalty for each month the tax stays unpaid (up to a total of 12% penalty, which does not include the initial 5% penalty).

Additionally, IRAS may pursue additional enforcement or judicial steps to recoup the unpaid tax.

Tax Incentives in General

The following table summarises the general tax exemption currently available to Singapore-resident businesses. When these tax exemptions are applied to taxable income, the effective tax rate for small to medium-sized Singapore businesses is dramatically lowered.

From YA2020 onwards, the following tax exemptions apply to newly established corporations in their first three consecutive YAs:

- Exemption of 75% on the first $100,000 of ordinary chargeable income. The first S$100,000 in taxable income for each of the first three tax filing years will be excluded from the 75% corporate income tax rate for newly registered firms that fulfil the following conditions:

- Singapore-based corporation

- a Singaporean tax resident (Please see below the tax residency of company)

- has no more than 20 shareholders of which at least one is an individual shareholder holding at least 10% of shares.

The above general tax benefits translate into relatively favourable tax rates for small- to medium-sized businesses. For instance, a typical Singapore resident firm with an annual taxable income of S$2,000,000 will be taxed as follows :

Effective Corporate Tax Rate

The above general tax incentives mean very attractive tax rates for small-to-midsize companies. For example, a typical Singapore resident company with S$2,000,000 annual taxable income will be taxed as below:

Income tax filings for incorporated companies in the first three years:

Income tax filing due date

For Singapore corporations, the corporate tax filing deadline is 30 November (for paper copy forms) and 15 December (for electronic forms) (for e-filing).

The business must file a comprehensive set of returns, which includes Form C, audited/unaudited financial statements, and tax computation. The Form C is a declaration form that a business uses to declare its income, whereas the tax computation is a statement that details the adjustments made to the net profit/loss as reported in the company's books in order to arrive at

Income tax basis period

Corporate income is calculated in Singapore using the prior year's figures. This implies that the base period for any Year of Assessment (YA) is typically the financial year ending (FYE) of the preceding financial year. For instance, in 2021, you will file a corporation tax return for the financial year ending between January 1, 2020 and December 31, 2020. Each year, your company's financial statements are created up to the financial year end (FYE).

Withholding tax

Singapore has implemented a withholding tax law (on certain types of income) to ensure the collection of tax payable to non-residents on income generated in Singapore. The tax withholding does not apply to Singapore resident companies or individuals. Under the law, when a payment of a specified nature is made to a non-resident company or individual, a percentage of the payment has to be withheld and paid to Income Tax Authorities. The amount withheld is called the withholding tax.

Singapore tax treaties

In general, a tax treaty between two countries describes how a company's revenue produced while doing business in both countries would be taxed by the respective country's authorities. In order to enable firms avoid paying two taxes on the same income, a tax treaty is essential.

More than 80 countries, including more recent additions, have signed tax treaties with Singapore. As a result of the agreements, Singapore continues to assist businesses in avoiding double taxation while also promoting and facilitating cross-border trade and investment activities.

Effective from YA2009, first year that Singapore would award unilateral tax incentives to Singapore-based businesses. In line with the new policy, all Singapore-based firms earning revenue from countries where double tax treaties do not exist will be eligible for a tax credit on their foreign income from such countries.

Frequently Asked Question